1. Apollo Just Paid $115M to Tell You Something

Apollo Global - $696B AUM, Wall Street suits, definitely not your average DeFi degen - wrote a nine-figure check for 9% of Morpho's supply in February 2026.

Same week: BlackRock listed its $2.2B BUIDL fund directly on Uniswap.

I'm not saying this to hype you up. I'm saying this because when two of the most conservative allocators on the planet make coordinated moves into DeFi lending infrastructure, they're telling you something about where rate spreads are heading - and if you're still hunting for the next emissions farm, you're playing a completely different game than they are.

This is what "Institutional Mode" actually looks like when it arrives. Not a press release. A $115M position in a lending primitive.

So where does DeFi lending actually stand in early 2026?

Total lending TVL sits around ~$60B+. The market hasn't exploded the way some 2024 predictions suggested - and honestly, that's fine. What's more interesting is who is in it and why.

The hierarchy has crystallized into three lanes, and they're not really competing with each other anymore:

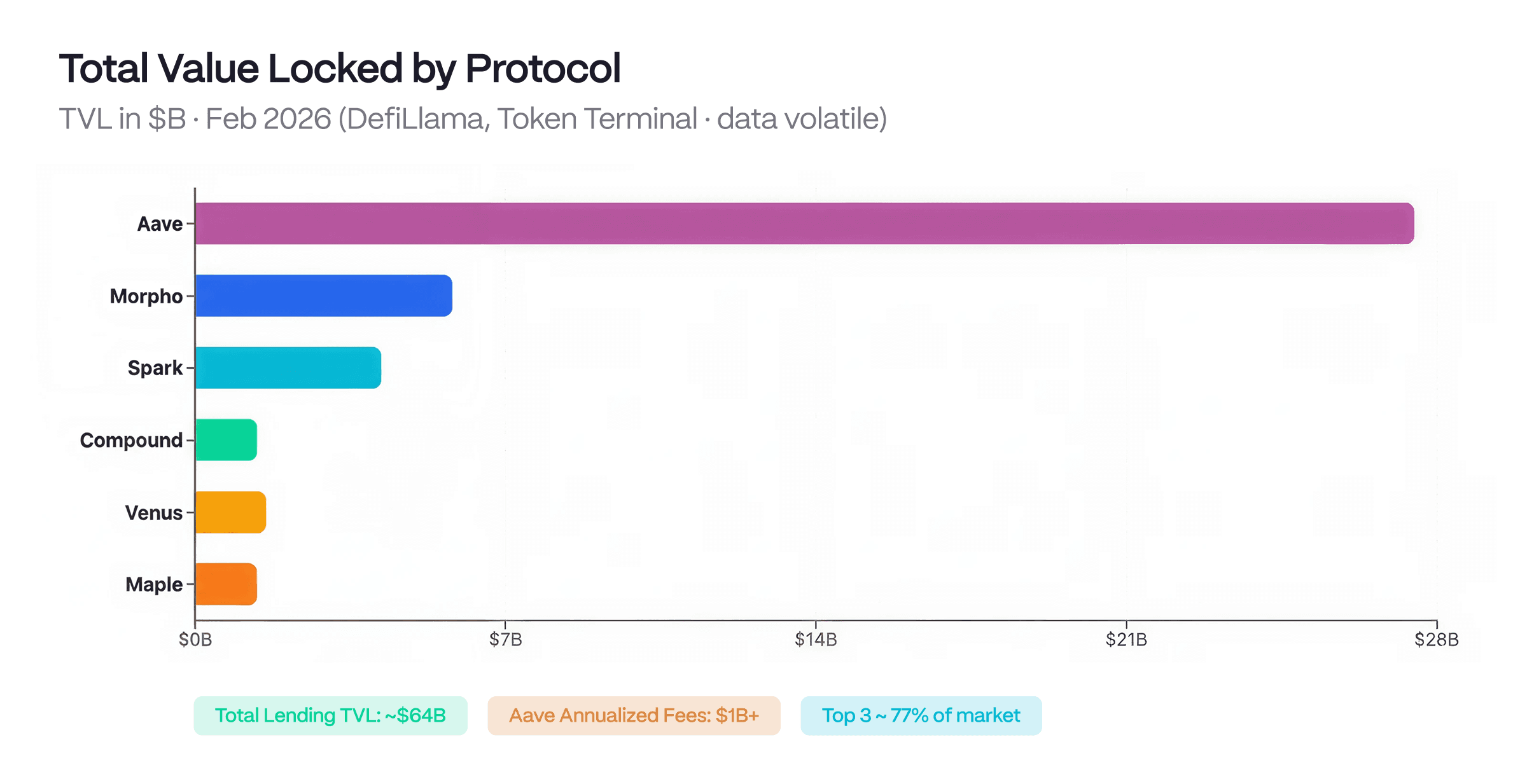

Aave is the infrastructure. $27.5B TVL, 50%+ market share, and V4's hub-and-spoke architecture is quietly becoming the credit layer for the whole multi-chain ecosystem. Institutions don't choose Aave for yield - they choose it because it's the deepest pool available and you can move $50M without surprises.

Morpho is the efficiency play. $13B in deposits by end-2025. The genius move wasn't the P2P matching - it was the "DeFi Mullet": fintech frontend, DeFi backend. Coinbase is routing $1.2B in consumer loans through Morpho on Base right now. Those users have zero idea they're interacting with a smart contract. That's how you scale.

Compound is the anchor nobody talks about. ~$1.25B in V3, zero hype, zero new token launches. And I'll explain exactly why that's actually a feature, not a bug.

Is this market saturated? No. We're still finishing the experimental phase. The next leg of TVL growth won't come from retail FOMO - it'll come from tokenized bonds and fintech apps routing billions through invisible DeFi backends. We're early in that, not late.

Figure 1. Lending Market Concentration. Aave owns the house, but Morpho is moving in fast. When the Top 3 control 77% of the market, the "experimental" phase is officially over - this is institutional consolidation.

2. The Mechanics: Where People Are Actually Making Money

Here's the honest version: most people in DeFi are still chasing APY numbers without understanding why those numbers exist. And the ones who understand the mechanics - they're the ones Apollo is competing with now.

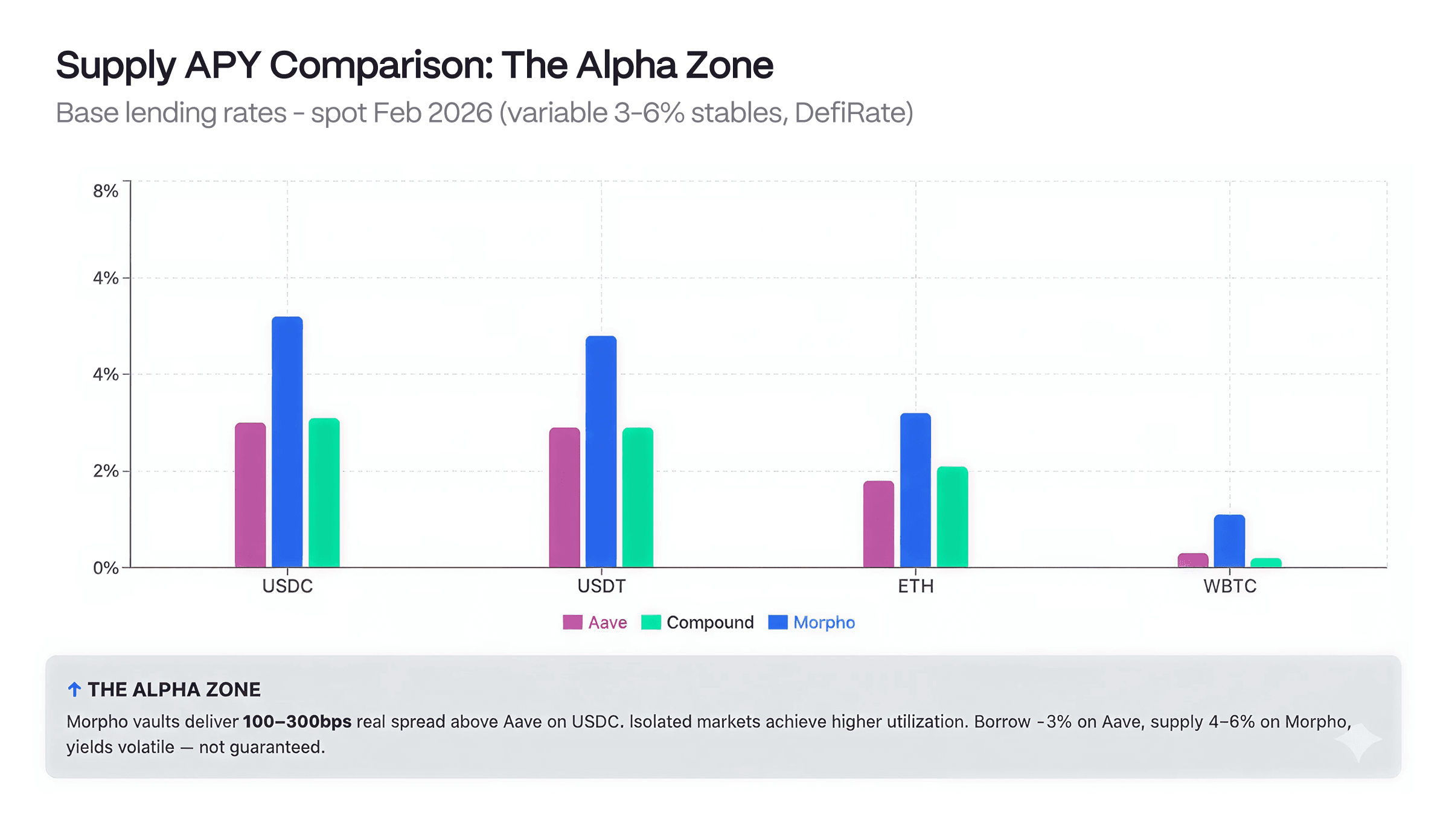

The Spread

There's a persistent yield gap between Aave and Morpho on USDC. We're talking 100-340 Вbasis points, consistently. Not a blip - structural.

Why does it exist? Simple:

Aave pulls passive, sticky capital. DAO treasuries, protocol reserves, conservative allocators who set positions and don't touch them for months. High supply relative to borrow demand → moderate utilization → compressed rates. Currently around 2.3% supply APY on USDC mainnet.

Morpho attracts active, concentrated capital. Institutional curators who run isolated vaults at aggressive utilization targets - think 85-90% utilization vs Aave's 60-70%. Higher utilization → higher rates paid to lenders. 4-6%+ on comparable USDC exposure.

The trade: borrow at ~3% on Aave, supply at 5.5% on Morpho. Pocket the 250bps delta. Scale to $10M and you're running a delta-neutral yield strategy that looks boring and prints money. The spread persists because moving large capital between protocols has real execution friction - not everyone can do this efficiently. That friction is the moat.

Figure 2. Yield Map: The Alpha Zone. This is the spread Apollo is betting on. A persistent 200-300bps gap on USDC isn't a fluke; it’s just Morpho running its engines harder (higher utilization) than Aave

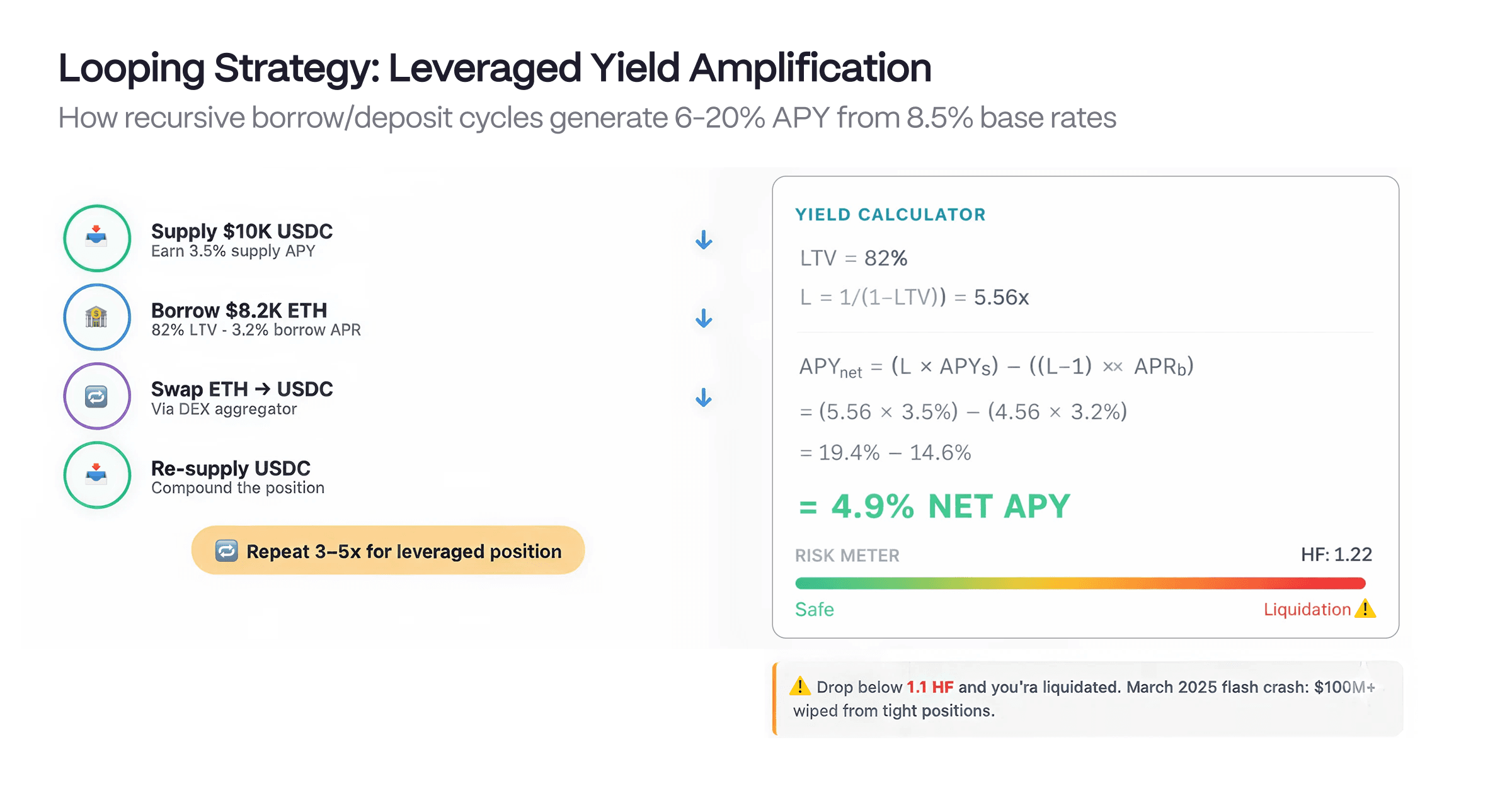

Looping - The Math Everyone Calculates Wrong

Looping (recursive borrowing) still generates serious yield. But it migrated entirely to L2s - because running the same loop on Ethereum mainnet costs $20-40 in gas per cycle, while on Bas e or Arbitrum you're paying under a cent. The strategy only makes sense when fees don't eat the spread.

Here's the formula people get wrong:

APY_net = (L × APY_supply) − ((L−1) × APR_borrow)

Where: L = 1 / (1 − LTV)

Real example using wstETH/ETH correlation (LTV 90% → 10x leverage):

Supply APY: 3.5% (restaking yield)

Borrow APR: 3.2%

Net: (10 × 3.5%) - (9 × 3.2%) = 6.2% on fully deployed capital

That yield is backed by actual borrowing demand and EigenLayer restaking - not token inflation. It's "real" in the way DeFi has been promising for years and rarely delivering.

But here's what most people miss: at 90% LTV with 10x leverage, a 2% move in the collateral/borrow asset ratio takes your health factor from 1.11 to 0.99. You're liquidated. Not maybe liquidated - liquidated. March 2025 flash crash demonstrated this live: $100M+ in positions wiped because people were running tight health factors on loops they thought were "safe" because the assets were correlated.

Smart money runs the same strategy at 82% LTV. The yield drops slightly. The sleep quality improves dramatically.

Figure 3. Leverage: High Stakes, High Reward. The math of "free money" until it isn't. High leverage looks great on paper, but watch that HF meter - don’t become a 2025 flash crash statistic. Execute on L2 or don’t bother.

Where the Yield Actually Comes From

Four sources, in order of importance in 2026:

Organic borrowing demand (65%) - leverage seekers, hedgers, institutions borrowing against RWA collateral

Protocol fees (15%) - Aave's GHO recycling, Morpho curator fees, Compound reserve capture

RWA/Treasury backing (12%) - tokenized Treasuries setting the risk-free floor at 4.5-5.5%

Token incentives (8%) - still exists, now additive rather than the main course

The transition from "ponzi emissions" to real economic yield isn't complete - but the direction is locked in. The 8% incentives number is the one to watch. When it hits zero, you'll know the market is fully mature.

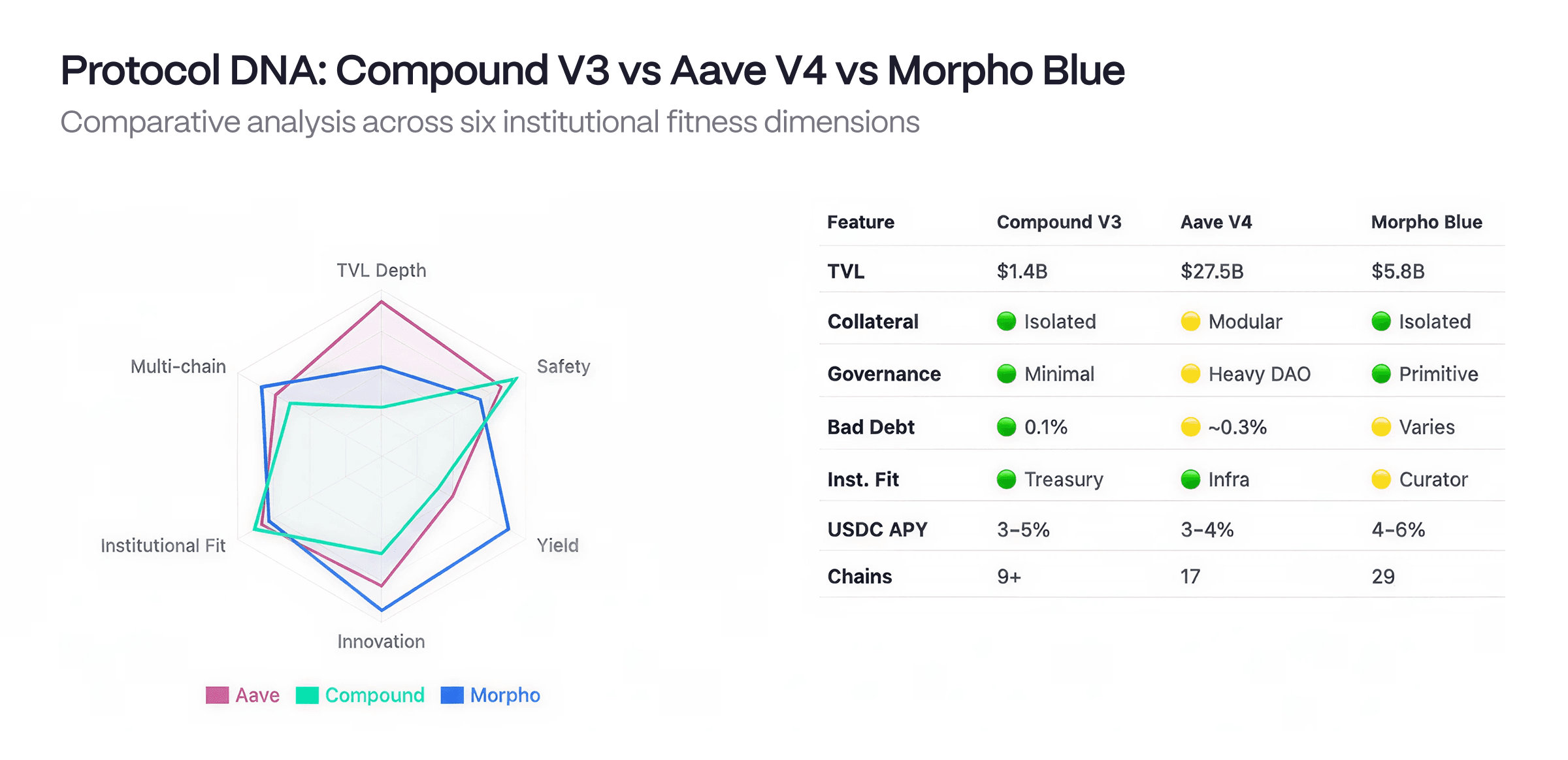

3. Compound: The Quiet One at the Table

People keep sleeping on Compound. I get it - no hype, no new token mechanics, no viral integrations. Just the same thing, working, every day.

But let me give you a specific scenario, because "it's reliable" is not an argument - it's a shrug.

It's Friday, 10 PM UTC. You need to unwind a $12M USDC position on Arbitrum. You check Morpho's best USDC vault - $8M in available liquidity at that hour. You can exit $8M clean, but the remaining $4M hits the utilization ceiling. Rates spike. Your exit degrades. You're negotiating with a smart contract at midnight and losing.

Compound on Arbitrum USDC: the single-base-asset architecture means the entire pool exists for one purpose - USDC in and out. At $12M you don't touch the ceiling. You exit at the rate you modeled, on schedule, no surprises.

That's not a narrative. That's architecture doing its job.

What "Comet" (Compound V3) actually does:

The core mechanic is isolated single-base-asset markets. Each deployment revolves around one borrowable asset only (USDC on Base, ETH on Arbitrum). Unlike the old pooled model - where a bad collateral listing could contaminate everything - Compound's risk is bounded by construction.

This is why Compound runs 0.1% bad debt versus the industry average of 0.3-0.5%. Not because they're lucky or conservative with listings. Because isolation prevents contagion by design.

What working inside the Woof growth program on Compound actually showed:

Deploying 70 new assets across 12 markets gives you ground-level data. Two things stood out:

The Chainlink SVR integration is criminally underrated. It captures MEV from liquidations and routes it back to the protocol instead of letting it leak to searcher bots. One of the cleanest mechanism designs in current DeFi - turns systemic risk into protocol revenue.

Compound's governance predictability is a builder subsidy. When you're constructing a composable vault that routes through Compound, you're not worried about a DAO snapshot at 2 AM flipping a risk parameter that breaks your position overnight. That stability isn't boring - it's worth money to anyone building on top.

My actual take: Compound isn't competing with Morpho for yield optimizers or with Aave for infrastructure scale. It's winning the "I need to know this won't break" use case. In institutional DeFi, that's the largest addressable market. Just the least glamorous.

Figure 4. Why I Call Compound the "Anchor". Compound won’t give you the highest APY, and that’s the point. Its "Safety" axis is a deliberate architectural choice - built to survive black swans that would break more "innovative" protocols.

4. What I'm Actually Watching - Two Obvious Things and One Nobody Has Priced

I don't do price predictions. I track where capital is structurally forced to move.

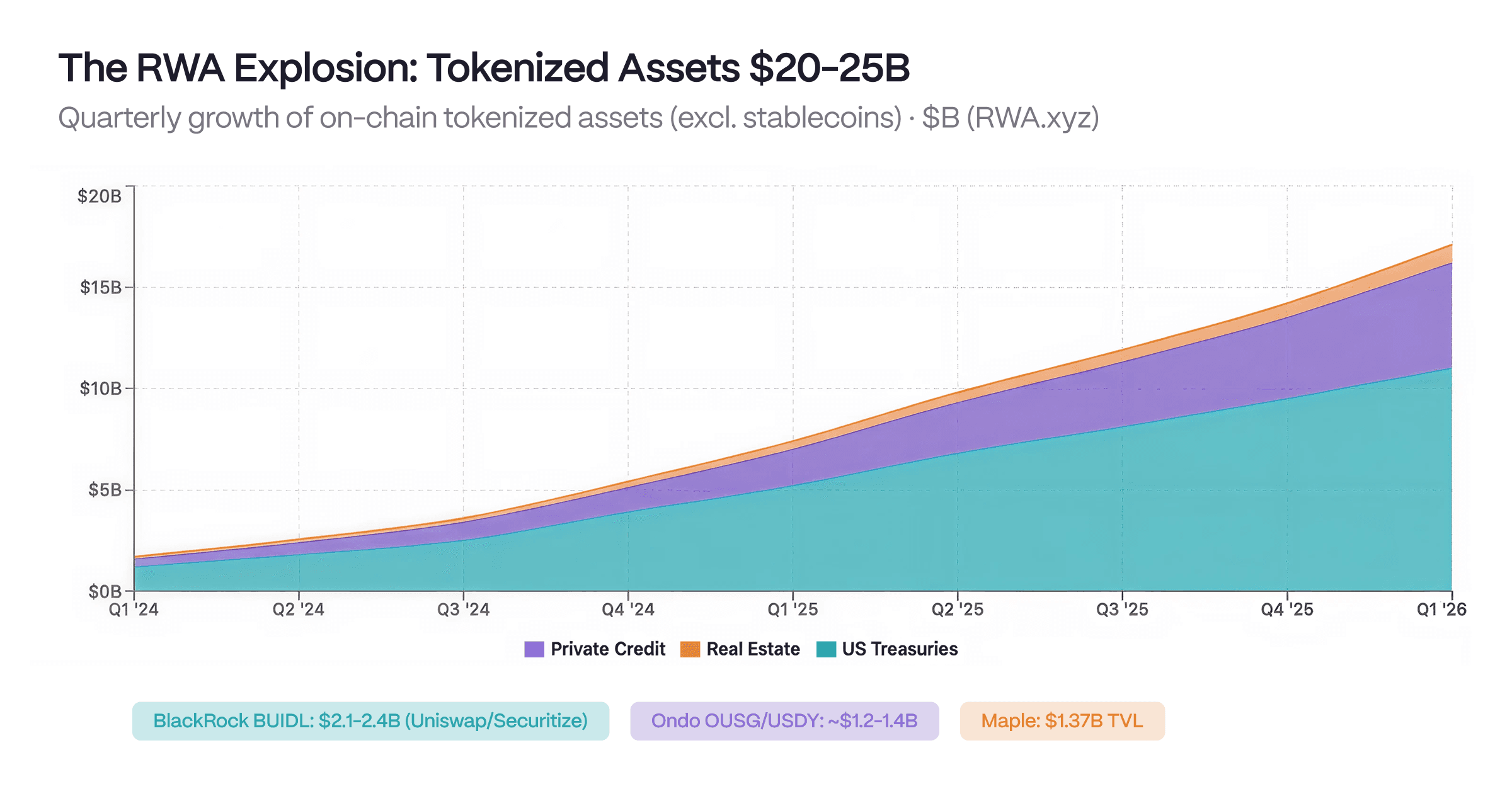

The obvious one: RWA composability

The tokenized RWA market crossed ~$20-25B. BlackRock BUIDL ($2.2B), Ondo ($1.4B), Franklin Templeton - these aren't experiments anymore, they're infrastructure. The next phase everyone's modeling: hold tokenized Treasuries → earn 5% risk-free → post as collateral on Aave/Morpho → borrow stablecoins → deploy elsewhere. Double-stacked yield on the same capital base. This is the "money lego" moment for traditional finance that DeFi has been promising since 2020.

Figure 5. The $25B Reality Check. Tokenized Treasuries are no longer a pilot project, they’re the new "risk-free" rate for DeFi. This is the base layer for everything we’re building in 2026.

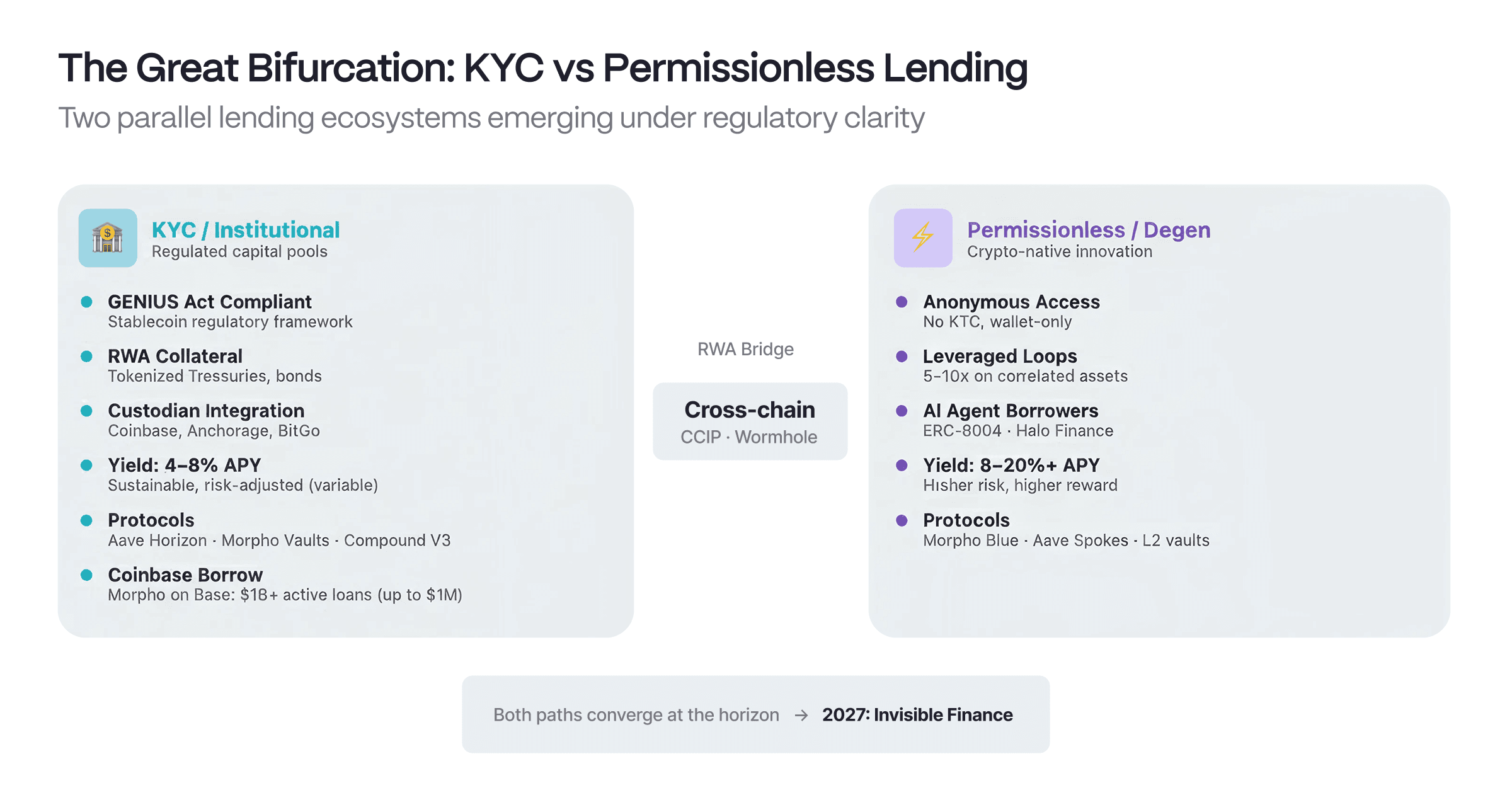

The one most people understand too simply: the regulatory fork

GENIUS Act in the US, MiCA in Europe. Yes, this creates a KYC/permissionless bifurcation - everyone's written about the two-lane market. What most pieces miss: the bifurcation creates permanent structural arbitrage. Regulatory constraints on institutional pools mean they'll systematically underutilize yield opportunities that permissionless capital can access freely. That spread doesn't close - it compounds. The more regulated capital enters DeFi, the larger the gap between what institutions can do and what you can do.

The one nobody has priced: AI agent borrowers

This is real and it's starting now. AI agents managing on-chain capital are becoming active borrowers - not as a roadmap item, as live protocol participants. They behave fundamentally differently from human borrowers: high-frequency position adjustments, precise health factor management, no panic in volatility, no hesitation at execution time.

Here's the problem: current lending protocols are parameterized for human borrowers. Liquidation thresholds, interest rate curves, oracle update frequencies - all calibrated for human reaction times. As agent capital scales, these parameters become mispriced for the actual borrower mix. The protocols that build infrastructure for non-human participants first - "Know Your Agent" (KYA) primitives, agent-optimized liquidation mechanics - capture a flow that's currently invisible to most market analysis.

It's a smaller market than RWAs today. But it's the one where being early actually matters.

The roadmap below shows how both regulatory paths eventually feed the same invisible fintech frontend - that's the endgame. Notice the third branch emerging for agent capital.

Figure 6. The Great Fork. Whether you’re in a KYC pool or a degen vault, we’re all heading toward the same "invisible" endgame in 2027. The only difference is the yield you’re allowed to capture.

The Bottom Line

Institutional mode didn't come gradually - it arrived, repriced the market, and most people missed it because they were still watching APY numbers instead of capital flow structure.

The protocols that win are determined by architecture: Aave owns depth and distribution, Morpho owns efficiency and the invisible backend play, Compound owns the "won't break when it matters" use case that serious capital actually needs and rarely talks about publicly.

The looping math is real. The spread between Aave and Morpho is structural, not temporary. The RWA composability is early innings. And the AI borrower angle is the one that could look obvious in 18 months.

Money moves toward efficiency and predictability at the same time. Understanding why - the mechanisms, not the narratives - is the only edge that compounds.

By Mykola Ilchuk (https://x.com/nikola_ilchuk) — R&D Technical Researcher at Woof Software. Looking for hidden opportunities for your protocol? We find them and build the solutions. Let’s build! (https://woof.software/build)