Amsterdam, 1774: The “Pre-seed” of the modern world. A merchant named Abraham van Ketwich did something the Amsterdam exchange had never seen before - he made investing boring. His creation, Eendragt Maakt Magt (“Unity Creates Strength”), became the world’s first modern investment fund. It didn't promise spectacular returns. It promised diversification, a modest yield, and, most importantly, the ability to sleep through the night without worrying about your money. The Dutch aristocracy loved it, not because it was exciting, but precisely because it wasn't.

250 years later, this “boring” idea manages $6.3 trillion in American money market funds alone. Nobody checks their money market balance every morning. Nobody joins a Discord to discuss “to the moon” strategies for Treasury bills. The money just sits there, it grows, and you forget about it.

This condition - where financial infrastructure becomes so reliable that the user simply forgets it exists - is the Boredom Premium. And it is likely the largest market opportunity that DeFi has yet to capture.

The Pattern Nobody Talks About

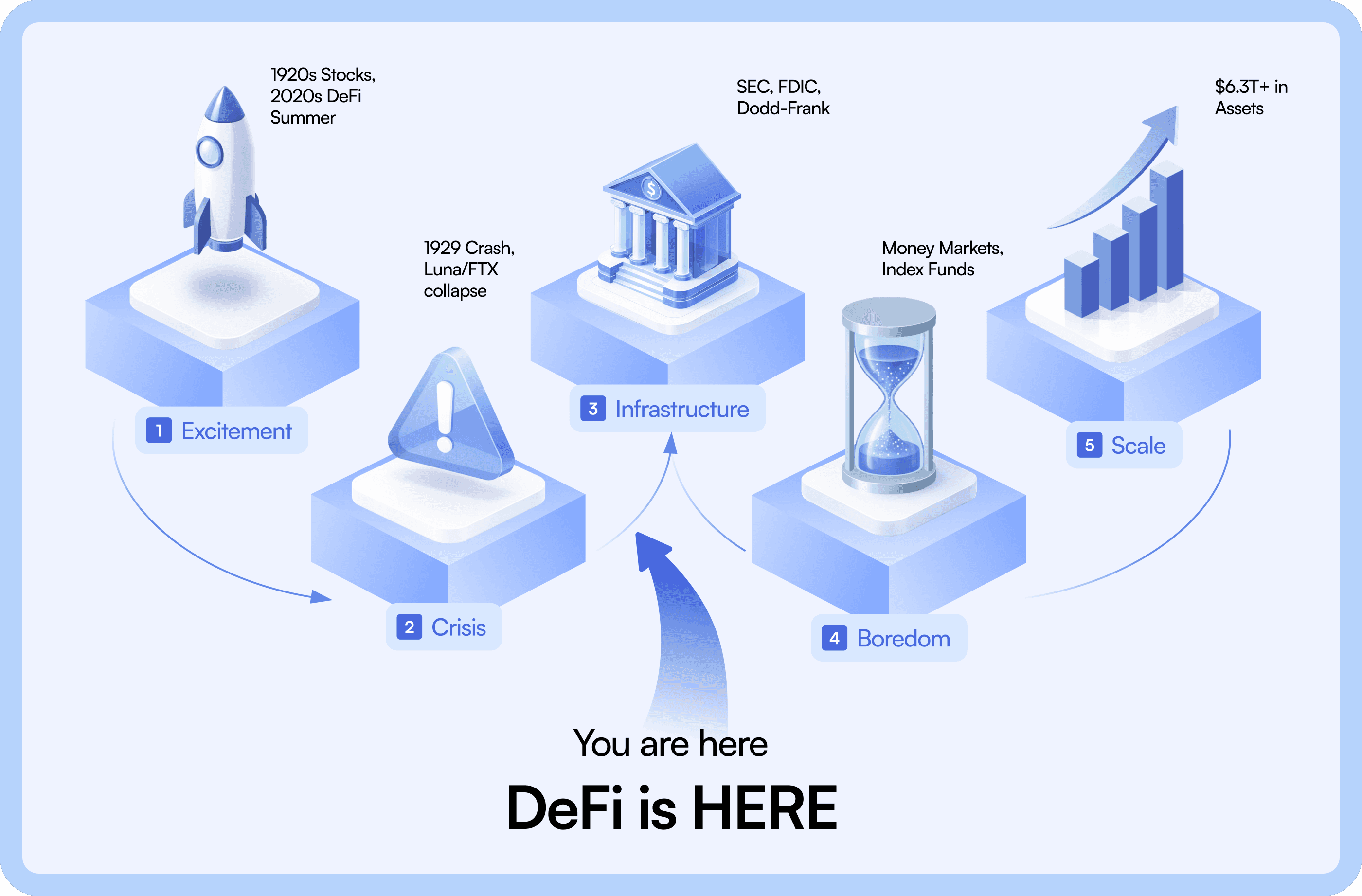

Every financial technology in human history has passed through the same five stages of the market cycle. No exceptions.

1920s, “Bucket Shops”: For the first time, ordinary Americans rushed to trade stocks, not realizing their “exchanges” never actually placed their orders on any market. The 1929 crash forced the creation of the SEC, FDIC, and federal deposit insurance. This was boring regulation that made banking safe for the masses.

1980s, “Junk Bonds”: Michael Milken (an American financier known as the "junk bond king" for his role in developing the market for high-yield bonds) argued that the market was underpricing yield. After a decade of euphoria, Drexel Burnham Lambert - the powerhouse Wall Street investment bank that fueled this entire junk bond craze - collapsed into bankruptcy. The result: rating agencies gained real enforcement power. Boring, but the system survived.

2000s, MBS (Mortgage-Backed Securities): The legend that “housing prices never go down”. Turns out, they do. The response: Dodd-Frank (2010 comprehensive Wall Street reform law that heavily increased regulation, stress-testing, and consumer protections) and TARP (2008 government bailout that bought toxic MBS and injected capital into banks). This kicked off the most tedious era in banking history. Banks are still paying for this boredom, and that’s exactly why they remain solvent today.

2020s, DeFi Summer: “Number go up”. Then Luna. Then FTX. Then Euler. The response: a graveyard of first-generation insurance protocols that collapsed under the weight of their own flawed tokenomics, and a wave of undercollateralized credit platforms (think Celsius or BlockFi) that blew up the moment real market stress tested their spreadsheets.

The pattern is immutable: Excitement → Crisis → Infrastructure → Boredom → Scale.

DeFi is currently stuck between Crisis and Infrastructure. The question isn't whether DeFi will become boring, it's who builds the rails for that boredom.

Figure 1.The 5-Stage Financial Technology Cycle

Cultural Code and the “Adverse Selection Death Spiral”

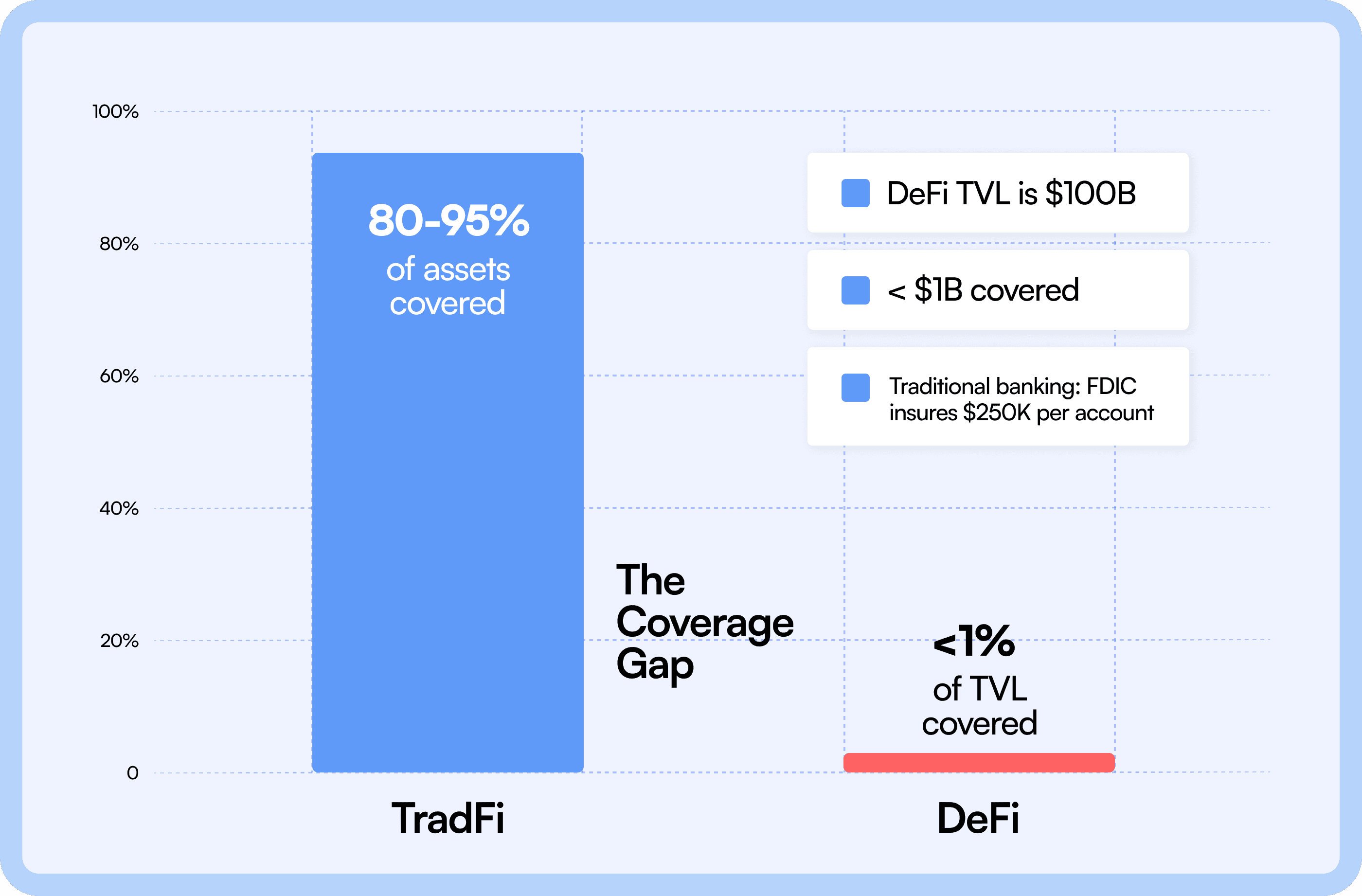

Why does nobody insure the thing they worry about most? We insure our cars, our houses, our teeth, and even our fantasy football teams. But we don't insure our capital in DeFi - the thing we worry about most. Less than 1% of DeFi TVL carries any form of coverage, while in TradFi, that figure is 80–95%. Billions of dollars sit in smart contracts without a single “parachute”. Not for lack of tools, but because nobody is buying them. The reasons are brutally simple:

It's painfully expensive (often eating 50-80% of your net yield).

The UX is fragmented (forcing users to hunt down coverage on secondary protocols).

The payouts are subjective (relying on opaque DAO governance votes rather than deterministic code).

But beneath these friction points lies a deeper, structural flaw where psychology and poor market design violently collide.

Figure 2. The Coverage Gap

This is where it gets interesting. Psychology and poor market design collide here. Historically, DeFi culture was built on an unwritten, binary code: you’re either completely bullish, or you shouldn't be here. For years, actively seeking downside protection was viewed by the crypto-native crowd almost as an admission of weakness - like showing up to a party and loudly announcing you think the roof might cave in.

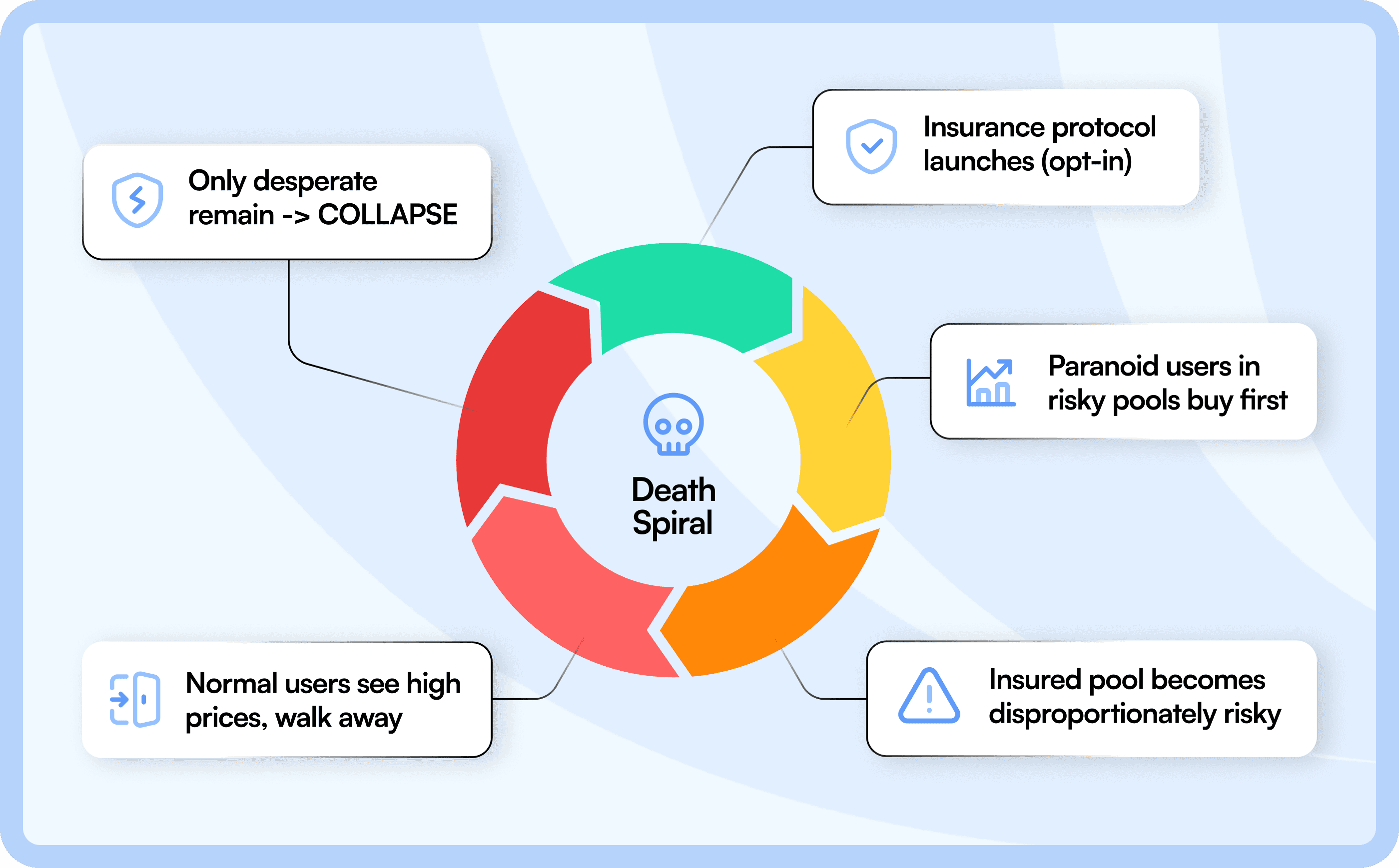

But while retail degens might enjoy playing financial roulette, institutional capital does not. The fact that 95–98% of DeFi capital remains uncovered isn't just a quirk of crypto psychology anymore; it's a symptom of a market that forces users to actively opt-in to their own anxiety. And mathematically, this opt-in model triggers a fatal economic chain reaction. It has a name: the Adverse Selection Death Spiral, which has killed every previous attempt to create DeFi insurance until today.

The mechanics of this collapse are mathematically inevitable:

You launch a protocol where coverage is strictly opt-in.

Who buys first? The highest-risk actors sitting in the most vulnerable pools-the ones actively expecting an exploit.

The risk pool becomes hyper-concentrated with toxic exposure. Claim frequency rises, forcing premiums to skyrocket.

Conservative capital in safe vaults looks at the 5%+ premium, realizes it destroys their net yield, and walks away.

Premiums climb even higher to compensate. Only the most desperate remain. The system collapses.

This isn't a theoretical model; it’s the literal post-mortem of the first-generation DeFi insurance market. Look at Nexus Mutual: $200M in reserves trapped behind 36-to-72-hour manual claims, subjective governance votes on payouts, and opaque underwriting. Look at what happened to InsurAce, Ease (Armor.fi), Unslashed, and Neptune Mutual.

When the 2022 stress tests hit (the UST depeg and FTX collapse), on-chain insurers faced roughly $34M in claims - about 90% of all historical payouts - instantly overwhelming their liquid capacity. Unslashed had written $400 million in coverage against a mere $90 million in capital. The B3i consortium, backed by 20+ global TradFi reinsurers, burned through $23M and went bankrupt without ever solving the core inefficiency.

Previous DeFi insurance wasn't killed by bad code. It was killed by a critical error in market design.

Figure 3. The Insurance Death Spiral

The Catalysis Play: Coverage as a Default Layer

Now imagine a different scenario. Coverage is embedded directly into the vault. By default. You deposit - you’re covered. Period.

In this model, adverse selection is flipped on its head. We aren't gathering paranoiacs into a single pool; we’re covering everyone. Retail and institutions, the cautious and the carefree. Risk is distributed across a broad base instead of concentrating among the anxious few.

The result: premiums drop, underwriter revenue stabilizes, and users don't have to "admit they're nervous" - the coverage is simply there. We call these Catalysis Covered Vaults: pools where downside protection is not a feature you buy, but a property of the vault itself.

Nobody “buys” FDIC insurance. You open a bank account, and your first $250,000 is covered. It’s not a feature of the bank; it’s a feature of the system.

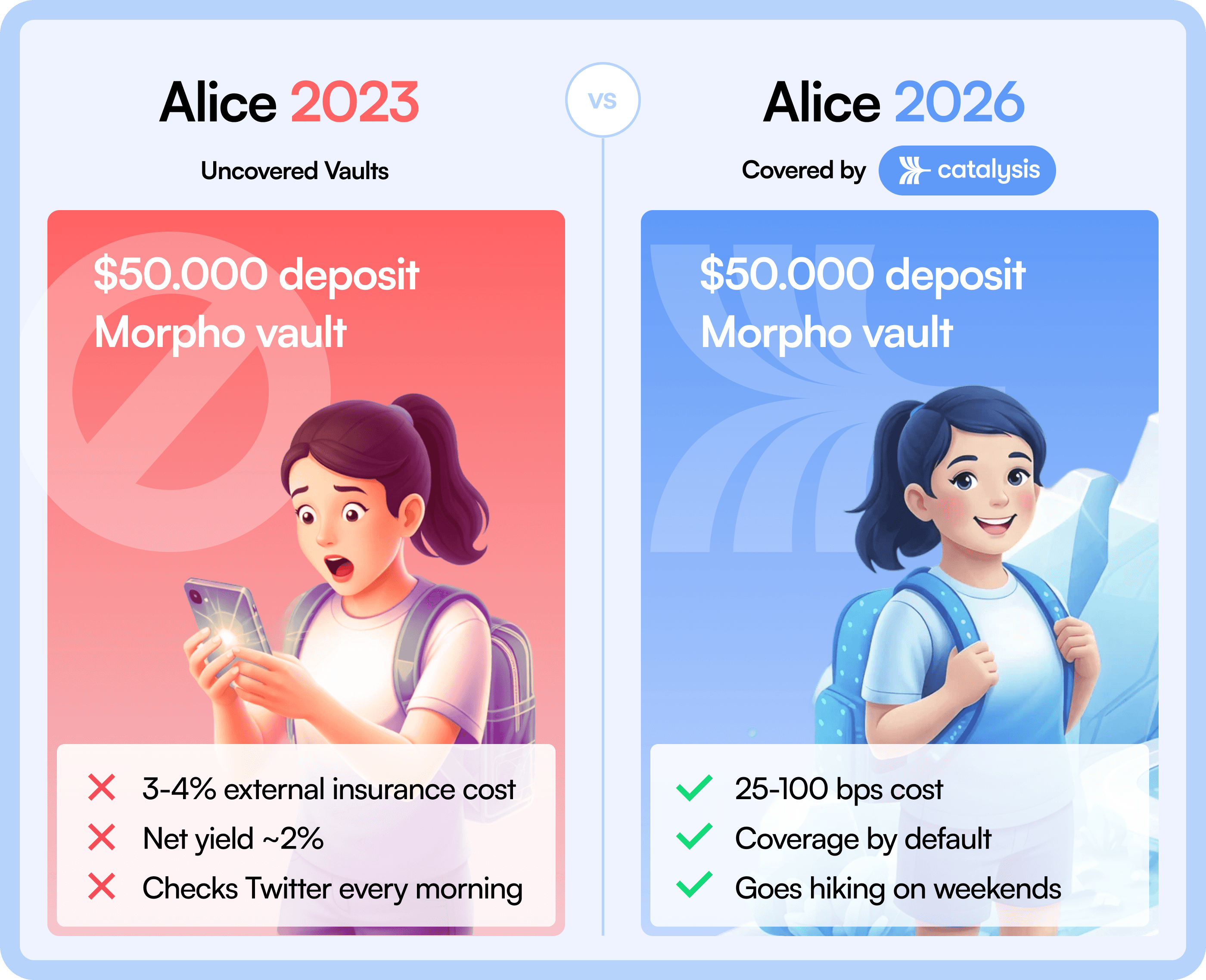

Figure 4. Alice 2023 vs. Alice 2026

Engineering the Boredom: The Invisible Infrastructure

Catalysis builds vault-native coverage that actually works because it removes human hesitation from the loop. Risk is isolated. Payouts are deterministic. No governance committees are debating your claim for three weeks - just code executing, slashing when predefined conditions are met.

If you want the deep dive into the exact architecture, how restaked capital secures the pools, and the math behind contagion-free CoverPools, we broke down the entire technical stack here: https://x.com/0xcatalysis/status/2021236666925494321?s=20.

What actually matters right now is what this looks like for the end user. And realistically, it looks like nothing.

There are no extra buttons to click, no premiums to manually calculate, and no secondary protocols to visit. You simply deposit your capital, and the downside is capped by default. For the user, the anxiety of DeFi is entirely abstracted away.

By making the complex risk-management machinery completely invisible, Catalysis isn't just launching another DeFi product. It is building the exact baseline infrastructure required to absorb the next massive wave of institutional liquidity.

The Trillion-Dollar Standard: Scaling New Financial Rails

In 2020, DeFi was a $13 billion market. Projections put it at $1.4 trillion by the early 2030s. But those trillions won't come from flashy APYs chased by crypto-native degens. They will come from corporate treasurers, pension funds, and family offices - people whose entire job is finding safe, boring yield. According to the Coinbase-EY 2026 Institutional Investor Survey, 43% of institutions plan to engage with DeFi protocols within the next two years, on top of the 13% already using them - and they aren't waiting for more exciting features. Their top three concerns tell the whole story: security (85%), regulatory uncertainty (84%), and compliance (81%). They're waiting for downside protection.The future of DeFi is about you not knowing that you’re using DeFi. In ten years, your money will sit in a DeFi vault, and you won't know it’s DeFi, and you won't care. That will be the ultimate win.

The signals are already here. Coinbase Earn now routes USDC through curated Morpho vaults. Kraken's DeFi Earn, launched in early 2026 with Veda infrastructure and Chaos Labs risk management, pipes retail deposits into Aave and Morpho without users ever touching a wallet. The pattern is consistent: users want yield, but they want it risk-adjusted - whether they're retail or institutional. This isn't new behavior. TradFi users have always accepted lower yield in exchange for downside protection. DeFi simply hasn't offered that natively and efficiently - until now. Covered vaults unlock that latent demand.

Catalysis is building the infrastructure that makes that boredom possible.

By Mykola Ulchuk - R&D Technical Researcher at Woof and Abishek Kumar - Founder & CEO at Catalysis

Contact @woof_software today!